RED III was meant to do for green hydrogen what no voluntary market has managed: manufacture demand. By mandating the use of RFNBOs in industry and transport, the directive was supposed to give Europe its most powerful demand-side lever, precisely in the sectors where direct electrification stalls.

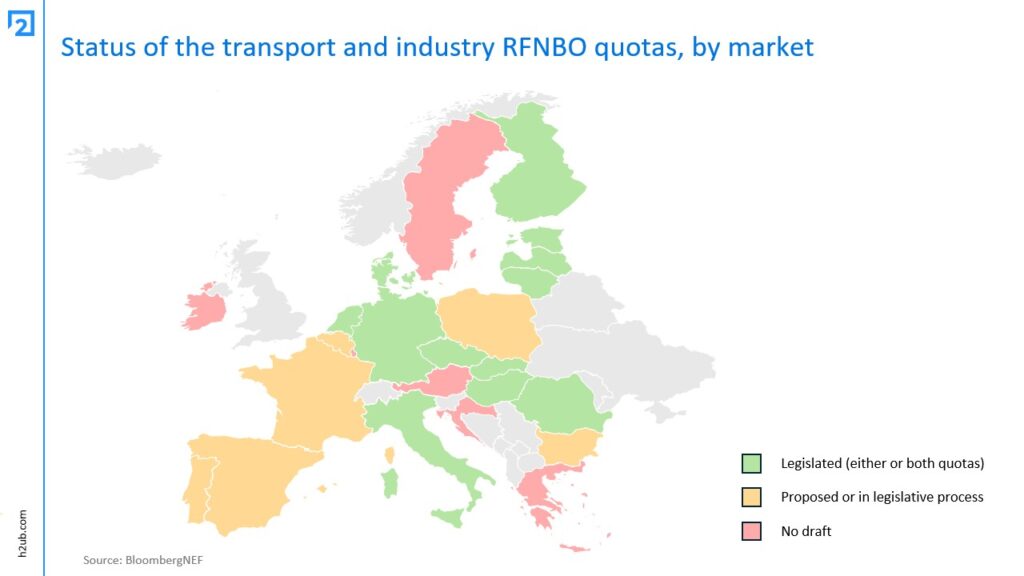

A year past the May 2025 transposition deadline, that lever is barely connected to anything. Only 13 member states have passed RED III quotas into national law, according to different sources; the rest are still drafting, consulting, or sitting on proposals. The delay has almost certainly had a negative impact on the hydrogen ramp-up across Europe because projects need bankable demand to reach FID stage.

Bankable demand only exists when quotas and penalties that are steep enough to change procurement behavior are actually written into law and can be enforced. Where legislation is still missing, that precondition isn’t met. And even if the precondition of national adoption is met, reaching the 2030 goals is still ambitious: Portugal, Denmark, Germany and the Netherlands have all transposed RED III into national law and thus are among the better placed countries in Europe. However, even these countries appear unlikely to meet the quotas they have passed.

A key flaw is enforcement. A quota is, in effect, a shadow price on hydrogen: it only binds if non-compliance costs more than compliance. Estimates put the threshold at roughly €10/kg. Below that, paying the penalty is cheaper than procuring green hydrogen at today’s costs, and most (?) parties simply pay it. Several countries have set penalties under that line. In those markets the quota exists on paper and is non-binding in practice, which defeats the entire mechanism.

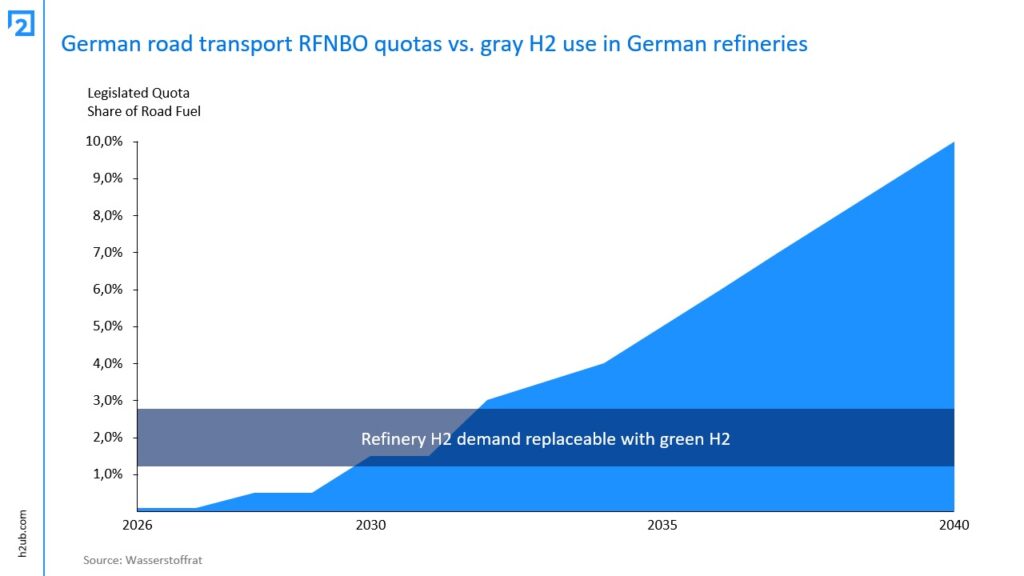

Germany is the clearest counterexample and a useful study in what a serious regime can and cannot do. The country has recently transposed RED III transport quotas into national law, creating one of the strongest green hydrogen quota regimes in Europe. The German quota is expected to raise demand for green hydrogen and derivatives in the transport sector, particularly through refinery use in the second half of the 2020s. Between 2026 and 2030, refineries are likely to be the main route for compliance because replacing gray hydrogen in refinery processes is the most direct way to meet the mandate.

That route has a ceiling, though. The refinery channel will likely be exhausted around 2030, because the volume of gray hydrogen that can realistically be replaced in German refineries is limited. After that, suppliers would increasingly need to use hydrogen-based fuels directly in transport or blend e-fuels into fossil fuels. This would raise cost pressure, especially if green hydrogen supply costs remain high.

Germany’s penalty level is also notable. At around €14,40/kg hydrogen equivalent, the penalty is high enough to make non-compliance economically unattractive for many obligated fuel suppliers. That gives the German system more credibility than lower-penalty approaches elsewhere in Europe. But it also means that if supply is scarce or expensive, costs will likely be passed through into fuel prices. This creates a political risk because higher fuel prices may lead to obligated parties lobbying for softer quotas or delayed implementation, as currently seen in the debate around SAF quotas under ReFuelEU Aviation. Any future quota revision would be a damaging signal for the hydrogen market, because bankability and offtake confidence weaken as soon as investors start to anticipate that binding demand targets could be relaxed again.

Germany’s transport quota is therefore an important first step. However, if Germany wants to secure its role as Europe’s leading hydrogen market, it now needs to move beyond transport and legislate clear RFNBO quotas for industrial hydrogen use, as required under EU rules. That would be an even larger lever than transport quotas, since industrial users already consume significant volumes of gray hydrogen, especially in refining, ammonia, methanol and basic chemicals.

Replacing this existing gray hydrogen with green hydrogen is often a more direct decarbonization pathway than pushing early hydrogen demand into fuel markets, where cost pass-through, customer acceptance and infrastructure readiness are more difficult. Industrial RFNBO quotas would therefore create a much clearer link between regulation and existing hydrogen demand.

For deeper insights get in touch with Alessandro Benassi:

alessandro.benassi@h2ub.com