Lately, one topic keeps surfacing in conversations across our ecosystem: SMRs as a future power source for hydrogen. Not because anyone believes they will fix the market in the next five years (spoiler alert: they won’t). But because they point to a problem the hydrogen sector tends to dodge: many industrial users do not just need low carbon molecules. They need reliable, local and steady volumes.

Here SMRs become interesting.

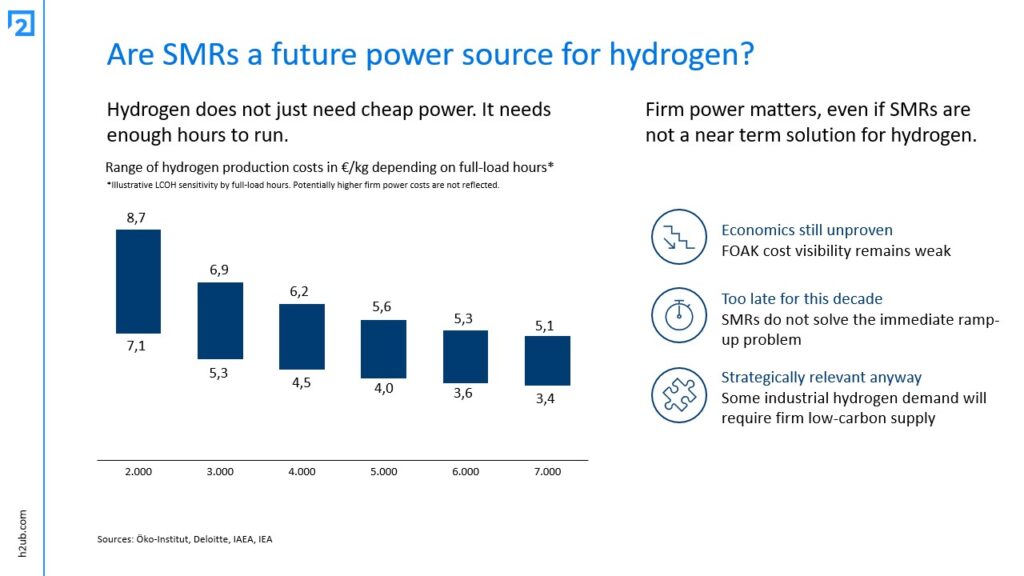

In theory, SMRs could provide firm low carbon electricity for electrolysis and, depending on the setup, usable heat for high-temperature pathways. That matters because higher electrolyzer utilisation and better overall system efficiency are two strong levers for lowering LCOH, especially in industrial use cases where continuous output matters more than occasional cheap production peaks.

The backdrop is shifting as well. The European Commission now has a strategy to bring Europe’s first SMRs online in the early 2030s. In the U.S., the Department of Energy selected the Tennessee Valley Authority (TVA) and Holtec for up to $800M of cost-shared support, private nuclear fission funding reached a record $1.3B by Q3 2025, and Google and Amazon have both backed nuclear as demand for reliable 24/7 power grows.

Still, a reality check is needed.

SMRs are not a near-term solution for hydrogen scale-up. Costs are still uncertain. Timelines are long. And the hydrogen market needs volumes well before SMRs are likely to contribute at scale.

But the real question is this:

Can hydrogen become an industrial backbone if we avoid the debate around firm, weather-independent power?

For deeper insights get in touch with Alessandro Benassi:

alessandro.benassi@h2ub.com